BANK SAVINGS AND CREDIT CARDS TO USE WHILST IN AUSTRALIA OR OVERSEAS

May 4, 2026 / by Marco / Categories : Finance

Choosing the right mix of bank cards is less about brand loyalty and more about assembling a toolkit that works across everyday life, local cash withdrawals, and foreign travel, all while keeping fees down and control up. Over time I have narrowed my wallet to a handful of cards that each serve a specific purpose, with one for daily mobile payments, another that shines when I am overseas, a low cost global card for currency flexibility, a couple of domestic accounts that help with savings and perks, and a straightforward credit card that delivers rewards and useful insurance. What follows is not simply a list, but a deeper look into how each card earns its place, how I actually use it in different situations, and what features make the experience smoother whether I am paying at a tap terminal or taking cash out of an unfamiliar ATM on the other side of the world.

ANZ PLUS AS MY DAILY COMPANION

ANZ Plus has become the card that stays in my mobile wallet, because it fits into the rhythm of daily spending without drama. The most immediate advantage is how it handles cash withdrawals at ATMX machines, the distinctive black ATMs that often tack on an extra fee. With ANZ Plus that surcharge is not charged, which is incredibly helpful when I just need quick cash without doing a mental cost benefit calculation at the screen. Since I keep the digital card on my phone, I can leave the physical card at home for most errands, and I still get the instant notifications and the budgeting features that ANZ has packed into the app. Those alerts that pop up the moment a transaction goes through are more than reassuring, they help rein in impulse spending by making every tap feel transparent and accountable.

Beyond the ATMs and alerts, ANZ Plus makes it easy to manage security on the fly. If I ever misplace the card I can lock it from the app in seconds, and when it turns up between the couch cushions I can unlock it just as quickly. Controls to disable tap to pay, restrict online purchases, or block overseas transactions are all there, which means I can tailor the card to the day rather than accept a one size fits all setting. For a local routine, from groceries to public transport to the occasional cash withdrawal at an ATMX, this blend of fee relief, real time information, and granular control is what keeps ANZ Plus at the top of my stack.

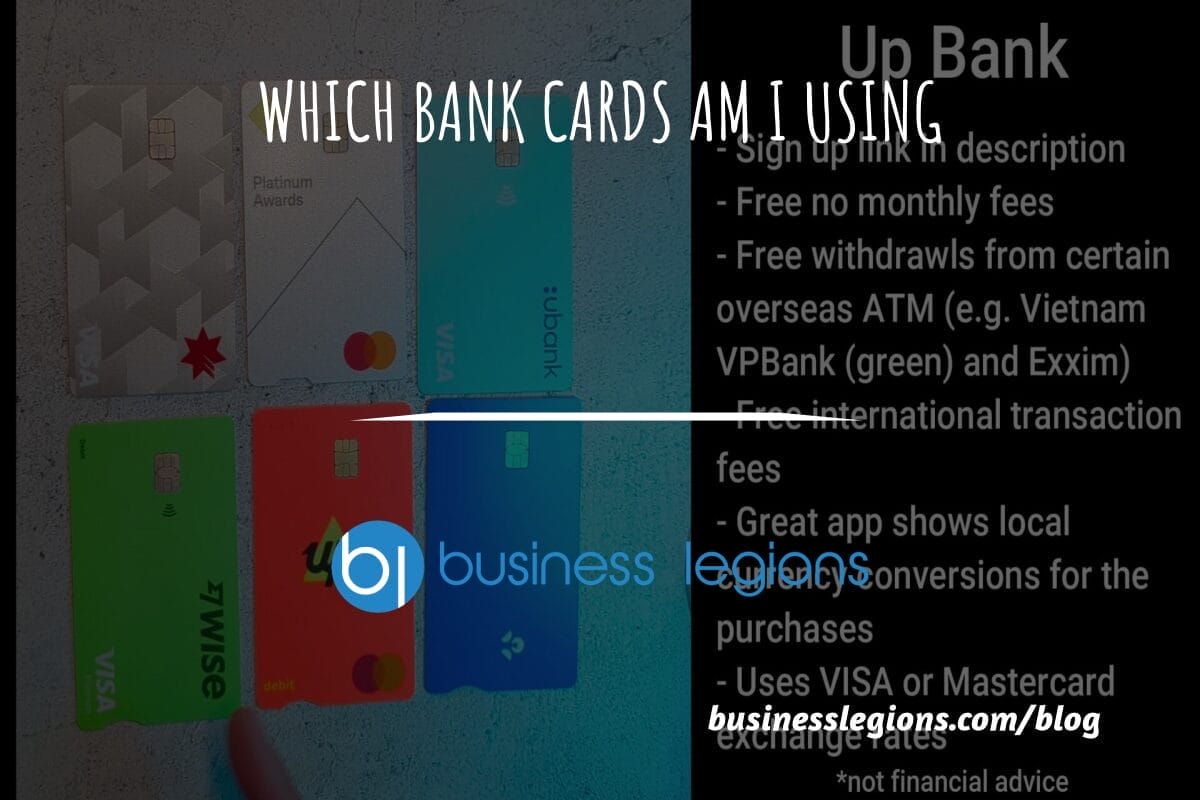

UPCARD WHEN I AM OVERSEAS

When I travel, UpCard steps into the spotlight. I have used it in Vietnam and found that certain ATMs let me withdraw cash without extra fees, which is a welcome change from the usual surprise charges that can nibble away at your travel budget. Specifically, I used VP Bank and ExSim ATMs and paid no fees on withdrawal, which matched the experience that many travellers report when they hunt for friendly local machines rather than taking the first option in a tourist area. Up does not add international transaction fees on top, and because the card processes payments at the network rate from Visa or Mastercard, you typically get a fair exchange when tapping for purchases. The result is that small coffee stops, ride hailing fares, and museum tickets abroad feel as straightforward as they do at home.

Up’s app also makes the experience of spending in a foreign country less opaque. There is a simple toggle that switches your view between home currency and local currency, so you can track exactly what you are spending without misreading zeros or misjudging conversions. Seeing both sides of the exchange helps you make confident decisions about whether to use the card for a larger purchase or take out cash, and it can guide you toward using the card where the network rate is likely to be better than what you would get at an airport bureau. I also make a habit of refusing dynamic currency conversion at the terminal, which is the prompt that asks if you want to be charged in your home currency instead of the local currency. Choosing the local currency keeps the transaction on the card network at a fair rate and avoids often inflated conversion offers on the merchant side.

WISE FOR LOW COST GLOBAL SPEND

Wise, sometimes misheard as Wyze, is the card I keep for flexibility when I am moving between currencies or when I want to lock in a favourable rate ahead of time. The account has no monthly fees, and you can use a virtual card without paying for plastic at all, which is convenient for online purchases or adding to a mobile wallet. If you do want a physical card for travel there is a small one off fee of around ten dollars, but the virtual option covers most day to day needs. Wise does not add international transaction fees either, and it allows a fair amount of ATM use for free each month, up to around four hundred dollars, before additional charges apply if you exceed that cap. For occasional cash needs this is plenty, and it is a nice complement to cards like Up when you are on the road for longer stretches.

What sets Wise apart is the ability to hold balances in different currencies and convert money when the rate looks attractive to you. If the exchange rate spikes in your favour on a particular day, you can convert into that currency and then spend from that balance later. This is not a promise of beating the market, but it is a practical tool to reduce the guesswork and give you more control than simply accepting whatever rate shows up at the moment of purchase. The Wise app shows mid market rates clearly, and transfers between currencies are transparent about any small fees, which helps to avoid that confusing blend of hidden spreads and extra charges that some services still rely on. I use Wise when I want to separate a travel budget into the currency of the destination, so I am not constantly translating amounts in my head and worrying about daily fluctuations when I should be navigating a metro map or exploring a new neighbourhood.

OTHER USEFUL ACCOUNTS THAT EARN THEIR KEEP

Some cards play more behind the scenes roles but are no less valuable. Ubank is one of those, and I think of it as a burner card when I am signing up for services that I am not sure I will stick with or when I want to ring fence a specific spending experiment. The exchange rates have been competitive and the interest rate on savings has been good, so I keep a few savings accounts within Ubank and label them for goals. The ability to create multiple savings accounts inside the one login is more powerful than it sounds, because it lets you separate groceries from travel or a future purchase without opening new accounts elsewhere. When a merchant seems flaky or a trial is more persistent than promised, I use the Ubank card with a low balance, so any unexpected charge attempt fails gracefully rather than drawing from my main spending account. Limits and locks in the app add another layer of safety and the mental clarity of knowing that the worst case is constrained.

NAB’s debit account, meanwhile, earns a place for the perks that come through the app, especially NAB Goodies. This is essentially a curated list of gift cards and offers that you can buy directly in the app, often with small discounts. If you already shop with a particular retailer, picking up a discounted gift card through NAB can shave a few dollars off everyday purchases without the hassle of chasing coupon codes. I like it for planned spending rather than impulse buys, so I will buy a gift card slightly under the total of a weekly shop or a known purchase, and then pay the balance with the card. That way the benefit is real and there is no leftover credit locked into an unused gift card. It is not a headline feature, but it is a simple way to stretch a budget and a good reminder that some debit accounts offer more than a card and a balance.

MY EVERYDAY CREDIT CARD FOR REWARDS AND PROTECTION

Despite my preference for debit cards day to day, a credit card remains a cornerstone for purchases where rewards and protections matter. The one I use charges a modest annual fee that is easy to justify because it earns reward points at a decent rate and includes travel insurance that covers the basics. Points are only useful if you can redeem them for what you value, so I tend to channel big predictable expenses through the credit card, like flights, accommodation, and recurring bills that accept card payments without adding a surcharge. When redemption time rolls around, using points for flights or quality merchandise beats the lower value options, and keeping a clear plan for those points stops them from languishing or being redeemed in a hurry for poor value.

The non points benefits are just as important. Most credit cards come with some level of purchase protection and a path to dispute transactions through the card network, which can be a fallback when a merchant is unresponsive. Travel insurance bundled with a card is not a universal safety net, and the policy details always matter, but it can be a helpful layer for trip cancellations, delays, or lost luggage when the card is used to book the travel. The discipline to pay the statement in full each month is what keeps the credit card an asset rather than a liability, and it means I can use it confidently for hotel deposits, car hire, or any transaction where a security hold is likely to be placed. Abroad, I still prefer to use debit cards with low or no international fees for everyday taps, but I reserve the credit card for transactions that benefit from the extra protections or require a credit card specifically.

A FEW PRACTICAL TIPS FROM HOW I STACK THESE CARDS

Putting all of this together, the pattern is simple but deliberate. At home, I lean on ANZ Plus in my mobile wallet for everyday taps and for cash at ATMX machines when I need it, because avoiding those ATM fees adds up over the months. When travelling, I bring UpCard to take advantage of fee free withdrawals at friendly local ATMs like VP Bank and ExSim in Vietnam, and I rely on the Visa or Mastercard network rate for fair conversions. Wise sits alongside those for its multi currency balances and the option to convert in advance when the rate looks right, which introduces a sense of control and helps keep a trip budget anchored in the destination currency. For online sign ups and situations where I want to limit exposure, Ubank acts as the burner, and its multiple savings accounts double as a neat budgeting system with clear buckets. NAB’s debit account earns its place by unlocking discounted gift cards through NAB Goodies, which is a small but steady way to make regular spending cost a bit less. The credit card gets the nod for big purchases, bookings, and any transaction where points and protections add material value, and then the balance is cleared before interest can take the shine off the rewards.

There are a few habits that tie the whole setup together and keep costs low. I always choose to be charged in the local currency when offered a choice at a terminal abroad, because that keeps the conversion at the card network rate rather than accepting a merchant rate that is usually worse. I also keep notifications on for every card, so if a charge posts that I do not recognise, I can freeze the card from the app immediately and investigate. When withdrawing cash overseas, I look for bank branded ATMs in well lit locations, and I test a small amount first to confirm that the machine does not spring a fee at the last moment. Within Australia, I remember that the black ATMX machines will not charge me when I use ANZ Plus, which gives me more flexibility about where I get cash if a branch ATM is not nearby. Before longer travel, I make sure my cards are added to my phone and watch, because contactless payments are widely accepted and losing a wallet is much less disruptive when the essential cards are still on my devices. Finally, I give myself a buffer by carrying at least two cards from different providers, so a network outage or an unexpected decline does not derail a day in a new city. If you use different cards for different purposes already, consider whether any of the roles here could strengthen your own toolkit, and if there is a standout card I should be using, I am always keen to hear what deserves a spot in the wallet next.

Marco / admin / 30 Nov

Writing day to day ramblings about making money, business, technology, sharing awesome deals and everything else that I know I'll forget. Follow my personal blog https://marcotran.com.au

I've recently also turned Vegan and started this website Veggie Meals - check it out

"When technology speaks for itself, that is art" - MT

Affiliate Compensated: there are some articles with links to products or services that I may receive a commission.

OTHER ARTICLES YOU MAY LIKE

BANK SAVINGS AND CREDIT CARDS TO USE WHILST IN AUSTRALIA OR OVERSEAS

Choosing the right mix of bank cards is less about brand loyalty and more about assembling a toolkit that works across everyday life, local cash withdrawals, and foreign travel, all while keeping fees down and control up. Over time I have narrowed my wallet to a handful of cards that each serve a specific purpose, […]

read more

Business Tip: Best way to send money overseas

Sending money overseas can be expensive if you are using the major banks. Over the past several years, I have been using a great service called OzForex for all my business and personal transactions. You can basically transfer money faster and for a lot less. Their fee is only AUD15.00 and I have found that their exchange rates […]

read more